fPlan has arrived. Canada’s choice for transparent, affordable advice-only expertise.

Unbiased, affordable advice-only financial planning services. Powered by Canada’s most advanced financial planning tools and technologies.

Why advice-only Financial Planning?

Canadians Pay for Financial Advice in One of Two Ways

In Canada, financial advice is most commonly priced as a percentage of assets under management. A typical advisory fee is approximately 1% annually and is charged in exchange for ongoing advice, planning, and service.This advice fee, while commonly bundled with other fees, is technically separate from the investment management costs of the investments held in the portfolio. However, because this advice fee is tied to portfolio value, it increases automatically as assets grow, regardless of whether the level of advice required changes.Advice-only financial planning uses a different pricing structure. Advice is treated as a professional service and billed using transparent flat fees. Clients engage planning services only when advice is needed, rather than paying an ongoing percentage tied to asset size.Over time, these two pricing models produce materially different financial outcomes, even when the quality of advice is comparable.

Quantifying the Difference Between the Two Models

Take the example of a $200,000 portfolio, where a 1% annual advice fee costs $2,000 in the first year. As the portfolio grows due to market performance, that cost increases proportionally.In contrast, when using an advice-only model that includes annual reviews ($250 annually) and periodic updates ($1,000 every 3 years, indexed to inflation), the cost savings are substantial. Over a 30-year period, this flat-fee structure results in an ending portfolio value that is more than $174,000 higher than the percentage-based alternative.To reiterate, this difference is not driven by market performance or investment selection. It arises solely from how the very same advice is priced.It’s a complex topic difficult to explain in a few lines, so we wrote an article about it. Here's more on advice-only vs. percentage-based pricing: Is Advice-Only Financial Planning Right for Everyone?

Our Professional Focus

At fPlan, financial planning is provided independently of investment management. We do not manage investments, receive commissions or earn referral fees of any kind.Our work is limited to advice, with fees based on scope and complexity rather than portfolio size. This structure allows us to be completely objective and impartial in all of the recommendations we make.

Who are we?

As a social enterprise, our mission is to challenge a financial industry that has remained largely unchanged for decades. In Canada, the wealth management landscape is dominated by a few traditional institutions that rely on the same high-margin, percentage-based models. We believe this status quo is overdue for a more transparent alternative. By using technology to keep our operations lean, we can provide top-tier professional advice at substantially lower costs.

Our advisory team is based out of Ontario and is comprised exclusively of experienced Certified Financial Planners® dedicated to providing unbiased, expert guidance.

We use secure, modern tools to keep our process efficient and our advice affordable, ensuring you receive high-quality financial strategies without the traditional industry markup.

We take a minimalist approach to your data, collecting only what we need. We employ the same high-level encryption standards used by major financial institutions.

Our firm operates virtually across Canada (excluding Quebec). We partner with you from home, using secure digital tools to achieve your financial goals without the commute.

The financial Planning process

❶

INITIAL DISCOVERY

Book a free 15-minute virtual consultation. This ensures our fee-only model is the right fit for your specific financial situation before any commitment.

❷

DIGITAL INTAKE

Action our digital intake survey to provide your preliminary financial information.

❸

SERVICE SELECTION

Sign the formal planning agreement and complete your purchase through our secure payment portal.

❹

DISCOVERY SESSION

Schedule your 90-minute financial planning discovery session. We’ll discuss your goals in depth and conduct a line-by-line data review.

❺

INTERACTIVE PRESENTATION

Within 10 business days of your session, we will contact you to host a 60-minute interactive virtual presentation of your completed financial plan.

Services & Fees

Financial Plan (Individual) | $ 899.00

A bespoke, comprehensive financial strategy designed to grow, protect, and simplify your wealth. This plan covers a full review of your asset allocation and savings strategies for retirement and other personal goals. We integrate general tax planning with dedicated retirement income planning to ensure your roadmap is efficient and actionable, covering these core areas and more.

Financial Plan (Couple) | $ 1,099.00

This comprehensive plan includes everything in the individual service, with the addition of income-splitting strategies and other elements unique to couples.

Advisory Meeting (60 minutes) | $ 250.00

A flexible 60-minute session with a tenured financial planner to discuss the financial matters most relevant to you. Topics can include general investment guidance, banking strategies, retirement planning, insurance, budgeting, or second opinions on financial decisions. Ideal for clients seeking targeted, expert advice without committing to a full financial plan.

FAQs

More questions? Email us directly.

- 1: As a social enterprise, we intentionally operate with very lean margins to provide professional planning to a broader range of Canadians. We mean to be an industry disruptor.

- 2: By automating many of our back-end administrative processes, we have removed the overhead costs that typically drive up service fees.

To ensure Canadian Data Sovereignty, our SaaS tools are operated through Zoho’s Canadian data centers, ensuring compliance with PIPEDA and PHIPA/PIPA standards. Virtual sessions are hosted on Microsoft Teams and protected by TLS 1.2/1.3 and AES-256 bit encryption for data in transit, ensuring that your audio, video, and screen sharing remain private and secure between you and your advisor.

Privacy Policy | Terms of Use | Disclaimer

© 2026 fPlan Advisory Inc. All rights reserved.

Legal & Privacy InformationLast Updated: January 28, 2026

1. Privacy Policy (PIPEDA Compliant)fPlan Advisory Inc. ("we", "us", or "our") is committed to protecting the privacy and security of your personal information. This policy outlines our practices in accordance with the Personal Information Protection and Electronic Documents Act (PIPEDA).Accountability: We are responsible for personal information under our control and have designated a Privacy Officer to oversee compliance.Information Collection: We collect information voluntarily provided by you (such as name, email, and financial data via contact forms or planning tools) and information collected automatically (such as IP addresses and cookies) to improve your experience.Purpose of Collection: Personal information is collected solely to provide financial planning services, respond to inquiries, and fulfill our contractual obligations to you.Consent: By using this website, you consent to the collection and use of your information as described. You may withdraw consent at any time by contacting us, subject to legal or contractual restrictions.Safeguards: We employ technological and organizational measures, including encryption and secure data storage, to protect your data from unauthorized access or theft.Openness & Access: You have the right to request access to the personal information we hold about you and to request corrections if it is inaccurate.2. Terms of Use & Advice-Only DisclaimerBy accessing this website, you agree to the following terms:For Educational Purposes Only: The content on this website is provided for general informational and educational purposes. It is not intended to provide specific personalized advice, including investment, financial, legal, accounting, or tax advice.No Securities or Insurance Sales: fPlan Advisory Inc. is an advice-only financial planning firm. We do not sell investment products, securities, or insurance. We are not registered as a securities dealer or insurance agent. No information on this site should be construed as an offer to buy or sell any financial instrument.No Professional-Client Relationship: Your use of this website does not establish a professional-client relationship. Such a relationship is only formed upon the execution of a formal written engagement agreement.Limitation of Liability: fPlan Advisory Inc. will not be liable for any damages arising from the use of, or inability to use, this website or the information contained herein.3. Trademark & Professional AttributionCFP® Marks: CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with flame design) are certification marks owned by Financial Planning Standards Board Ltd. (FPSB) and used under license by FP Canada™.Qualified Associate Financial Planner™: QAFP®, Qualified Associate Financial Planner™, and the QAFP logo are trademarks of FP Canada™.Ownership: All website content, including text, logos, and graphics, is the property of fPlan Advisory Inc. unless otherwise noted and is protected by Canadian copyright laws.

Blog

Is Advice-only Financial Planning Right for Everyone?

By Julien Bouchy-Picon, CFP® | January 29th, 2026

In Canada, the dominant way financial advice is priced is by charging a percentage of assets under management (later referenced in this article as "AUM"). This model is not inherently wrong, but it ties the cost of advice to portfolio size rather than to the complexity or scope of the advice itself, as advice-only financial planning does. Over time, it's bound to result in a pricing structure that is weakly connected to how financial advice is actually delivered.

After 15 years in advisory roles across the financial industry, I’ve seen how effective financial advice can materially improve outcomes for individuals and families. The value of advice in general is certainly not in question. The question is: do the fees paid for that advice reliably reflect the work being done by the advisor and the value brought forth to the client?

That question is precisely what led me to launch fPlan.

How Financial Advice Is Commonly Priced in Canada

Under the AUM model, an advisor’s compensation increases automatically as a client’s portfolio grows. If equity markets rise and a portfolio increases by 20% in a good year, the fee paid for advice rises by the same amount, even if the client’s financial situation is unchanged.

The issue is that portfolio size and financial complexity are not the same thing. A portfolio commonly grows due to market performance alone, without any increase in planning complexity. Yet the advice fees charged scale regardless. From a pricing standpoint, this creates a direct mismatch between fees and the value of the advice.

Why Performance Does Not Justify Advice Fees

I've heard investment performance being cited too often as justification for higher fees. This rests on a fundamental misunderstanding of how advice is priced. In many retail investment products, particularly mutual funds, the reported fee (known as the Management Expense Ratio or "MER") combines two separate components:

The investment management fee

A trailing commission that compensates the advisor for advice and service.

In other words, the advice fee is completely unrelated to the performance of the portfolio. Investment returns and advisory work are economically distinct services. In fact, many fund providers offer versions of their funds that exclude the ~1% advisor fee, but they're not made available on all platforms.

A Useful Analogy: Real Estate Commissions

If a home sells for $1,000,000 one year and $1,200,000 the next, a percentage-based commission paid to a real estate agent increases by 20%, even if the transaction itself is materially the same. Were services underpriced in the first year, or overpriced in the second? It is difficult to argue that the value of the service scaled precisely with the sale price. The same logic applies to advice fees in financial industry that rise solely due to market appreciation.

Transparency Is Improving — and That Matters

Canada’s Client Relationship Model (CRM) reforms which mandate greater disclosure requirements from financial services providers have made great strides over the years. The next phase, expected in 2026–2027, will further expand reporting on total costs which will be visible on client statements. As investors see the total fees paid, expressed in absolute dollar terms as opposed to ambiguous percentages, it becomes easier to evaluate whether those costs are proportionate to the advice received.

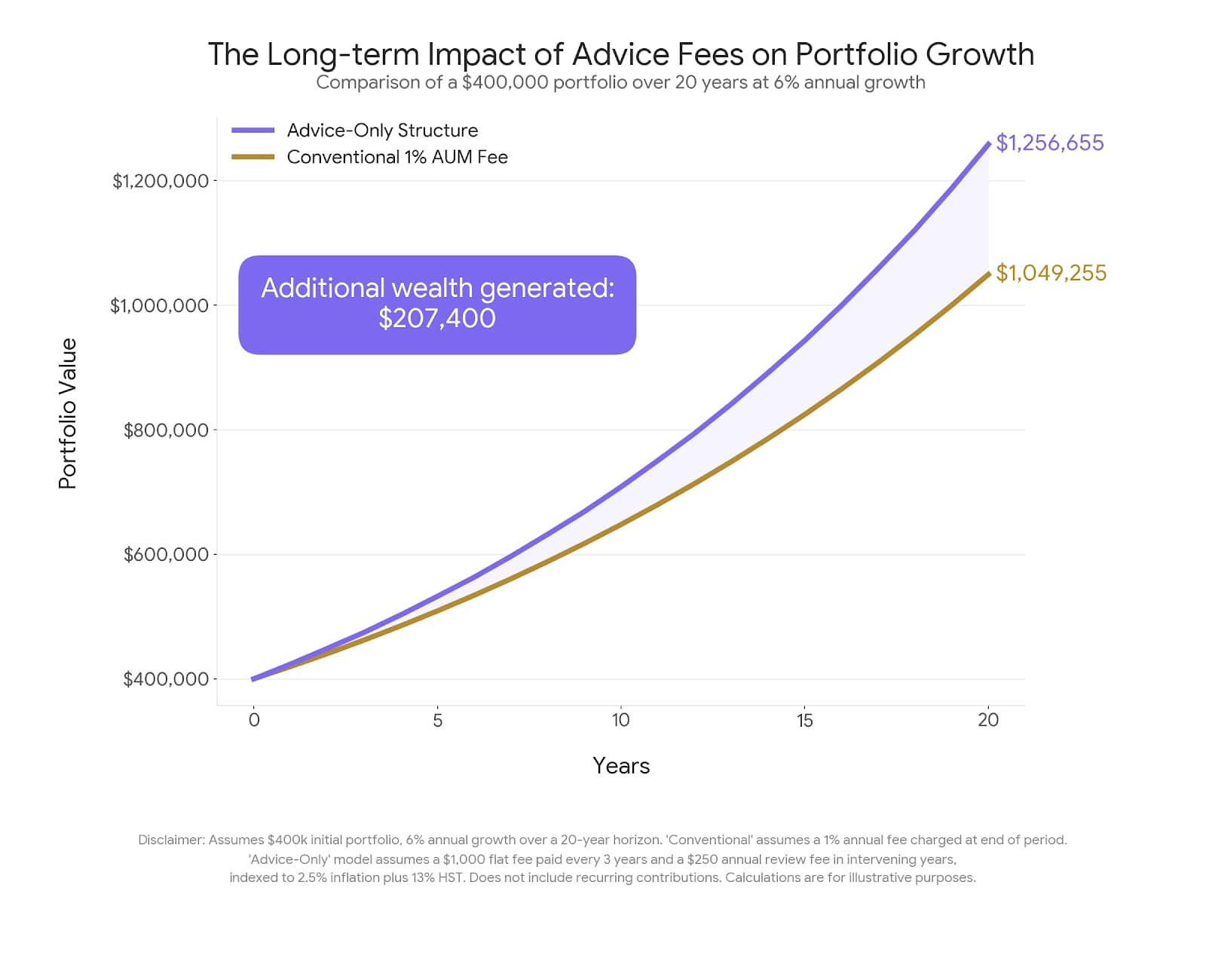

Let's Quantify It

To illustrate the long-term impact of advice fees, consider a $400,000 portfolio earning a 6% average annual return over a 20-year horizon.When using a traditional 1% AUM model, the total fees paid over two decades amount to $139,314, resulting in a final portfolio value of $1,049,255. In contrast, an Advice-only structure (which includes a $250 annual review fee + a $1,000 triennial financial plan update) costs just $14,707 over the same period, allowing the final portfolio to grow to $1,256,655.The resulting difference is staggering: by choosing an advice-only model under these assumptions, you would save $124,607 in fees for the same level of advice, and generate an additional $207,400 in total wealth. This wealth gap of over $207,000 occurs because of the "opportunity cost" - every dollar not spent on a commission remains in your account to compound over time.And this example does not even consider recurring investment contributions which would further increase the savings from a fee-only / advice-only model.

Why Advice-Only Financial Planning Aligns Cost With Value

Flat-fee financial planning is about aligning price with work. Fees are linked to complexity rather than market performance, similar to how accountants or real estate lawyers charge for their expertise. A larger portfolio does not necessarily imply a more complex financial situation, just as a smaller portfolio does not imply simple planning needs.

The Reason fPlan Exists

The purpose of fPlan is not to criticize traditional models, but to give Canadians a clearer way to evaluate whether the fees they pay are commensurate with the advice they receive.As investors become more aware of the true dollar cost of advice, I believe demand will grow for pricing models that are easier to understand and more directly linked to the service provided.That belief is the reason fPlan exists

Our Advisory Team

Julien Bouchy-Picon, CFP®

Julien is a Certified Financial Planner with 15 years of experience in Canada’s financial industry, most of it spent advising high-net-worth clients at RBC Royal Bank. His work has focused on retirement strategy, tax efficiency, investment structure, and estate planning.

In 2026, Julien founded fPlan Advisory Inc. after early-retiring from RBC at age 38. The decision was deliberate: to step away from product-driven advice and build a planning-first practice centered on clarity, independence, and long-term decision quality. fPlan operates on an advice-only basis, with no asset management, commissions, or embedded conflicts.Julien has a particular interest in early retirement planning, retirement income design, and evidence-based investing. His philosophy is pragmatic and analytical, with a strong bias toward passive portfolio construction and disciplined financial systems.Julien is currently completing an MBA in Business Analytics at the Sprott School of Business. Outside of work, he spends his time hiking with his wife and dog, and on track days at Calabogie.

SUCCESS!

Thank you for entrusting fPlan with your information. We’ve received your secure intake form. Please keep an eye on your inbox for next steps.

Privacy Policy | Terms of Use | Disclaimer

© 2026 fPlan Advisory Inc. All rights reserved.